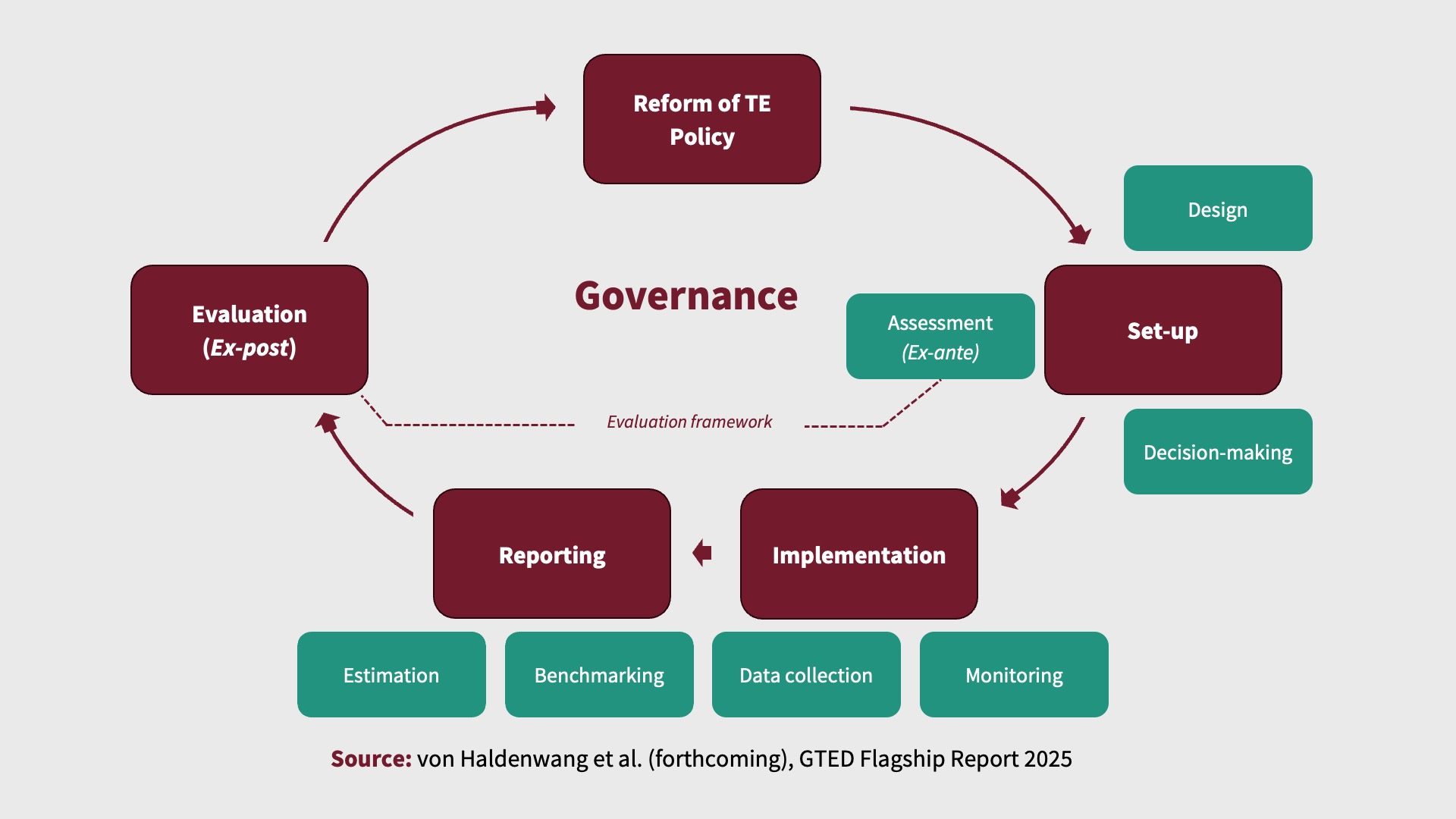

Tax expenditures (TEs) undergo a policy cycle that spans five interconnected stages: set-up, implementation, reporting, evaluation, and reform. Actions taken at each stage influence outcomes in other stages, making coherence across the cycle essential.

The SET-UP phase involves designing new provisions and deciding on their introduction. This stage should be informed by ex-ante assessments to assess expected costs and impacts and curb the proliferation of ineffective or overly expensive TE provisions.

A robust evaluation framework should be established from the outset to guide both ex-ante assessments and ex-post evaluations and maintain coherence over time. This helps define objectives, identify target groups, shape provisions design, and lay the groundwork for data collection and future evaluation.

IMPLEMENTATION covers the administrative side of tax expenditures, including data collection, estimation, and continuous monitoring. Effective implementation depends on coordination between the tax administration, the ministry of finance, the statistical office, and other relevant stakeholders to ensure reliable and consistent information.

REPORTING combines revenue forgone estimates with information that allows policymakers and the public in general to understand the fiscal costs, objectives and relevant features of TEs in use. A key element is defining the benchmark tax system, which allows for the proper identification and estimation of TEs. Information on policy objectives, beneficiaries, and legal references should also be provided. Reporting should be regular, comprehensive, and comparable over time.

Ex-post EVALUATION offers a deeper look at the performance of TEs by assessing whether objectives were met, while also considering cost-efficiency, broader externalities and, ideally, the performance of TEs compared to alternative policy tools. Evaluations range from empirical cost-benefit analysis and other types of impact assessments to less data-intensive methods such as distributional analysis or qualitative reviews.

Finally, the REFORM stage draws on the results of evaluations to improve or dismantle TEs. Reforms might involve modifying eligibility, redesigning TE provisions, or simply eliminating provisions that have proven to be ineffective, overly costly or even harmful. Yet, reforms often take place as a complex process that is highly dependent on political economy aspects and includes stakeholders such as ministries and the legislative, as well as business associations and civil society organizations, among others.

Sound governance throughout the policy cycle includes ensuring clear roles, effective rules, adequate capacity, and ultimately, accountability and evidence-based decision-making.